In 2025, the crypto market did not replicate the widespread frenzy of 2021 in terms of price action, but it underwent a profound structural "realignment." Mainstream assets were gradually integrated into compliant asset allocation frameworks, driven by ETFs and institutional capital. Stablecoins and on-chain infrastructure penetrated cross-border payments and capital market settlements under regulatory tailwinds like MiCA and the GENIUS Act. Meanwhile, the pathways for on-chain liquidity, user behavior, and risk pricing were quietly being rewritten.

This year resembled more of a relay station in crypto's transition from a "high-volatility asset" to a "long-term infrastructure" role. While thematic narratives ebbed and flowed, only those underlying structures directly embedded in capital flows, information pricing, and risk management processes proved capable of weathering cycles.

In this report, rather than summarizing all changes across the crypto industry, we intentionally focus on four main themes considered to have higher long-term value density and structural significance:

Exchange + Chain

Wallet + Stablecoin Payment Card

Information Financialization of Prediction Markets

Decentralized Perpetual Contract DEXs

Their common characteristic is that they either control capital and user entry points or directly participate in the market's repricing of information and risk.

Consequently, they are more likely to accumulate network effects and moats over subsequent cycles, rather than being fleeting thematic rotations.

I. Exchange + Chain: Four Models in the Era of Vertical Integration

1. Phenomenon: A Panoramic Comparison of the Four Major Exchange Chains

By 2025, exchange-built blockchains had moved from an exploratory phase into a mature stage of differentiation, forming a complete business loop: "Traffic Entry → On-Chain Applications → Ecosystem Tokens → Listing Feedback."

Three representative combinations—

Traffic Empire Model: Binance × BNB Chain

Compliance-First Path: Coinbase × Base, OKX × OK Chain

Institutionalized Deep Integration: Bybit × Mantle

| Dimension | Binance × BNB Chain | Coinbase × Base | Bybit × Mantle | OKX × OK Chain |

|---|---|---|---|---|

| Exchange Scale | Largest industry volume, leading in transaction and user numbers. | Leading compliant exchange in the US, high number of verified users and active trading. | Top global exchange, rapid growth in spot and derivatives. | Significant volume, relatively cautious, clear compliance strategy. |

| Public Chain TVL & Activity | High TVL, strong DEX trading and stablecoin usage, millions of daily active addresses. | TVL rising rapidly, active DeFi and on-chain trading. | Moderate DeFi TVL, growing bridged liquidity. | TVL ~$20M, minimal real on-chain activity. |

| Ecosystem Funding | Established massive Builder Fund, investing across multiple sectors. | Multiple accelerators and builder programs, continuous developer support. | Deep executive involvement in governance, combined with incentives and VIP systems. | Launched $100M X Layer Ecosystem Fund. |

| Listing & Traffic Synergy | Forms a "Traffic → Public Chain → Listing" flywheel, ecosystem projects receive rapid listings and liquidity support. | No significant linkage observed | No significant linkage observed | No significant linkage observed |

| Product Integration | Deep integration: low gas, MEV protection, routing & incentives bridging CEX and chain. | Base App, embedded wallets, and other products create a global user entry point. | Fee discounts, Vault products, RWA focus create a unified experience. | OK Wallet offers smooth experience, internal ecosystem still in early stages. |

| Strategic Positioning | "Traffic Empire": Using exchange traffic to feed the chain and project ecosystem. | Compliance-first + Developer-friendly + Institutional trust path. | Deep institutional integration, building a CeFi–DeFi flywheel around RWA. | Strategy pending, shifted from OK Chain to X Layer in 2025. |

| 2026 Outlook | Continue scaling and accelerating, strengthening CEX-chain integration. | Continue attracting Web2 teams and developers, deepening ecosystem. | Continue doubling down on RWA and institutional capabilities. | Narrative fully shifts to X Layer, needs further clarification. |

BNB's Initiatives Are Particularly Noteworthy

| Initiative | Mechanism Design | Synergistic Effect | Key Data |

|---|---|---|---|

| Binance Alpha Traffic Diversion | 0.01% ultra-low fee (1/10 of CEX) + points rewards + priority token deployment on-chain | CEX users actively bridge assets to BNB Chain for airdrops | $182.6M net inflow in 3 months, stablecoin market cap 70B→140B (+100%) |

| Gas Fee Waiver Lock-in | Zero-fee stablecoin transfers extended to Jan 31, 2026, avg gas dropped to 0.05 gwei (-98%) | User assets remain on-chain longer, more suitable for trading vs. withdrawing to CEX | $14B stablecoin peak locked, supporting DeFi liquidity |

| Meme Ecosystem Empowerment | Four.meme partnership + $1M prize pool + CZ tweet ignition | Positioning BNB Chain as a "low-cost meme launchpad" | $335M daily meme trading volume, Four.meme daily revenue $1.43M surpassing Solana's Pump.fun |

| Aster DEX Support | Deep integration with Binance Wallet + YZi Labs backing + high-leverage perps | Capturing traders migrating from CEX to on-chain | $6.6B daily perp volume, $1.261B TVL, significant share of global perp DEX market |

BNB Data Validation

Retention Effect:

Stablecoin market cap doubled from $7B peak to $14B (+100%)

Cumulative addresses exceed 700M, 4M daily active users

Application Prosperity:

Meme ecosystem: Four.meme daily revenue peaked at $1.43M, cumulative volume $20.5B

Aster DEX: $6.6B daily perp volume, cumulative volume $867B

Business Validation:

Q3 single-quarter fee revenue $357M (highest since Q1 2023, 4th among all chains)

Annualized fee revenue ~$154M, 60% to validators + 40% BNB burn

Three Keys to Synergistic Effects

1. Depth of Vertical Integration: Binance Alpha is not just a "token listing platform" but a bridge for pre-deploying CEX liquidity on-chain—users actively bridge assets for airdrops, completing the "CEX trader → on-chain user" conversion.

2. Retention Mechanism Innovation: The zero-gas policy "soft-locks" user assets on-chain (cost advantage vs. CEX internal transfers). $14B in stablecoins becomes foundational liquidity for DEXs like PancakeSwap, forming a "lock → liquidity → volume → fees" positive loop. However, it's worth noting that further exploration is needed on how to better keep capital on-chain.

3. Application Layer Value Capture: The Meme+Aster dual engine creates $816K daily application layer fees (1.87x chain fees), validating the "application prosperity → chain value increase" synergy logic. Compared to Base's 5.6x application/chain fee ratio, BNB Chain focuses more on chain fee capture.

II. Wallet + Payments: The Year of Non-Custodial Payment Cards, Stablecoins Become Core

The most significant trend in the wallet industry in 2025 was the collective integration of USDT/USDC payment cards (U Cards), bridging the "last mile" from on-chain assets to global consumption. Monthly crypto card spending surged from $14.6M-$17M in January to $91M-$105M in December (525%-600% YoY growth), with a November peak of $406M. Mainstream solutions like MetaMask Card, Trust Wallet×Oobit, Binance Web3 Wallet×Oobit, and Coinbase Card now cover over 80M+ global Visa/Mastercard merchants, marking wallets' transition from "self-custody tools" to "digital lifestyle payment gateways." Annual stablecoin transaction volume of $9T provides massive infrastructure support for payment cards.

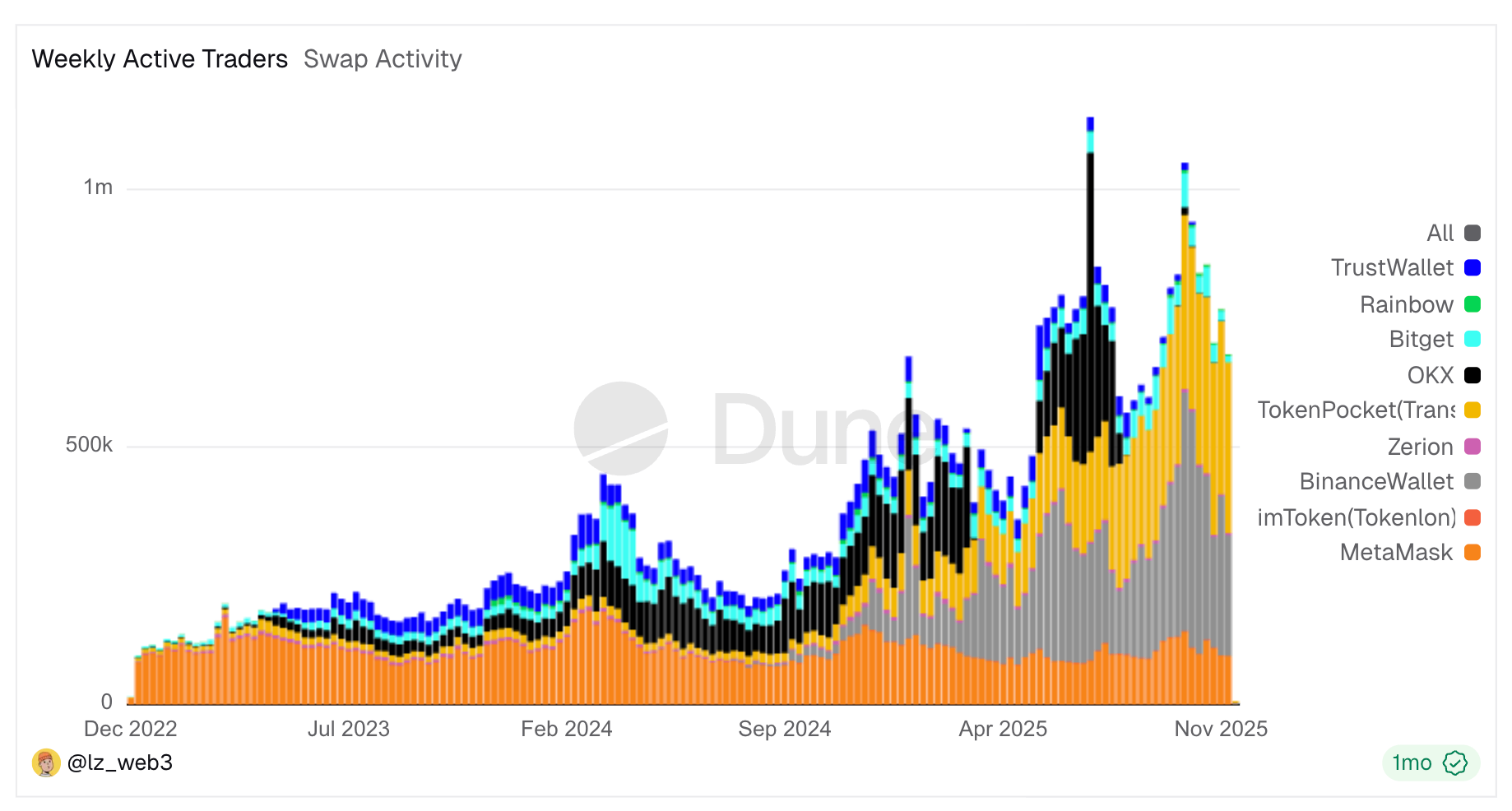

1. Current Crypto Wallet Usage Ratio and Market Landscape

Mainstream Wallet Market Share

Based on 2025 quarterly on-chain swap revenue data (as a proxy for activity), the leading wallet landscape is as follows:

User Growth Trends

Surge in Downloads: Global crypto wallet downloads in 2025 approached the historical peak of 2021, indicating a new adoption cycle. MetaMask, with over 30M MAU, remains in the top tier by user scale, with its trusted user count consistently nearing all-time highs.

Market Concentration: The top 5-7 wallets dominate the market share. Exchange wallet expansion plans are notable (Binance Wallet, OK Wallet, Bitget Wallet, etc.). Phantom, benefiting from the Solana ecosystem boom, achieved revenue overtaking, forming a dual-power structure with MetaMask across EVM and Solana ecosystems.

2. Core Wallet Use Cases: Trading Dominates, Diversification Accelerates

Primary Use Case Distribution

Based on 2025 on-chain data and wallet feature usage statistics:

| Use Case | Share / Data | Representative Wallet Features | Key Data |

|---|---|---|---|

| Trading / Swap | Dominant position | On-chain swap, perpetual contracts | MetaMask annual swap revenue $325M, Bitget monthly swap $900M |

| Stablecoin Payments | 30% of on-chain volume | Transfers, cross-border remittances | Monthly payment volume $10.2B (Aug 2025), +70% YoY |

| DeFi Interaction | Continuous growth | Staking, yield products | Participation +4% YoY, Trust Wallet Earn TVL $155M+ |

| Social / dApps | Emerging scenarios | Embedded wallet applications | Privy data shows social apps 53%, games 11%, AI products 8% |

Detailed Usage Data Analysis

Trading Category Absolutely Dominates:

Bitget Wallet monthly on-chain swap reached $900M, perpetual contract volume $5B (+291% YoY)

DeFi vs. CeFi perpetual trading ratio increased to 18.7x, indicating on-chain derivatives boom

Wallets have become primary swap venues, with built-in trading features seeing explosive usage

DeFi Yield Products Rapid Growth:

Bitget Wallet Earn quarterly volume $200M (10x YoY growth), primarily stablecoin products

Phantom supports on-chain staking & PSOL (97% of swap/trading volume on Solana)

Trust Wallet stablecoin Earn TVL over $155M, added products like RWA tokenized stocks

Stablecoin Payments as New Infrastructure:

On-chain stablecoins account for 30% of total transaction volume (TRM Labs data, excluding DeFi/gaming to focus on payments)

Monthly payment volume reached $10.2B (Aug 2025), annualized $1.22T, +70% YoY

Emerging markets (Nigeria, India) are primary growth engines, driven by cross-border remittance and daily payment needs

Emerging dApp Scenarios:

Embedded wallets (Privy, etc.): social apps 53%, enterprise apps 17%, games 11%

New features like prediction markets, high-leverage perps (up to 200x) proliferating in leading wallets

Wallets evolving from "tools" to "platforms," integrating trading, DeFi, payments, social, and other full-scenario capabilities

3. Mainstream Wallets Integrate U Cards: Collective Explosion of Non-Custodial Payment Cards

In 2025, we saw mainstream wallet projects collectively integrating U Cards and crypto payments:

Mainstream wallets are collectively launching non-custodial payment cards: funds remain in your on-chain wallet, converted to fiat via Mastercard/Visa networks only at the moment of swiping.

Typical structure is "Wallet App + Compliant Issuing Partner + Card Network + KYC/On-ramp Service" (e.g., Baanx, Bridge, Lead Bank, Mastercard/Visa, Stripe), accessing existing payment systems without sacrificing self-custody.

MetaMask Card follows a multi-chain/multi-stablecoin, global coverage, and high cashback route; Phantom Cash focuses on Solana-based USD cash accounts, initially targeting the US; Solflare Card specializes in self-custodial USDC spending on Solana, targeting the European market.

2024–2025 became the concentrated爆发 period for such cards. With Apple Pay/Google Pay integration, the path for crypto assets to move from "on-chain savings only" to "daily card spending" has been established.

| Project | Product Features (Key Points) | Supported Assets / Networks | Card Type & Fees/Cashback | Partners | Launch Timeline | Coverage Regions / Eligibility |

|---|---|---|---|---|---|---|

| MetaMask Card | Non-custodial mechanism: Funds stay in user wallet, instantly converted on-chain at spend; multi-chain self-custody payments. | Tokens: mUSD, USDC, USDT, wETH, EURe, GBPe; Networks: Linea, Solana, Base, etc. | Virtual Card: 1% cashback; Metal Premium Card: 3% USDC cash Latest News Flash More Recommended reading More |